Two Years, No Pay Cheque: The Portfolio I Built to Live Off

Built so that sitting still is the rational move, not the brave one, and still waiting for the year that proves it.

In the spring of 2024, in a rented flat in Turin, Italy, I sat down to design the portfolio I would have to live off. I had invested for 25 years by then, but always with a salary underneath me. I was on my way out of a large global family office, and for the first time the only account on the line would be my own, with no pay cheque at the end of the month to soften a bad period, no committee to share the blame.

A portfolio you have to live off stops being a scoreboard and becomes the thing that has to pay the bills while it goes nowhere for months. The design took a month and 4 versions of a spreadsheet. Living inside it has been the work of the 2 years since. What those years have not brought is a bad one: I have never sat through a 60% drawdown on this book with no pay cheque coming in, and I don’t know how it holds. I’m not going to pretend otherwise.

Nobody sits through months of red because they were born calm. They sit through it because the portfolio was built so that sitting still is the rational move rather than the brave one, and with no salary behind you that difference is the whole game. It comes down to what you own and how well you know it, how you get paid to hold it while nothing happens, and what you have trained yourself to feel when the screen is ugly. Lose any one and the other two eventually break. I set out the bones of this in No Pain to Begin With. What follows is the design underneath.

Holding power isn’t a personality trait you’re born with, like being tall. It’s manufactured, on purpose, before you need it.

Start from the goal, not the position

Most individuals build a portfolio from the position up: a name they like and a chart that looks ready. I build it from the goal down, and the order is most of the edge.

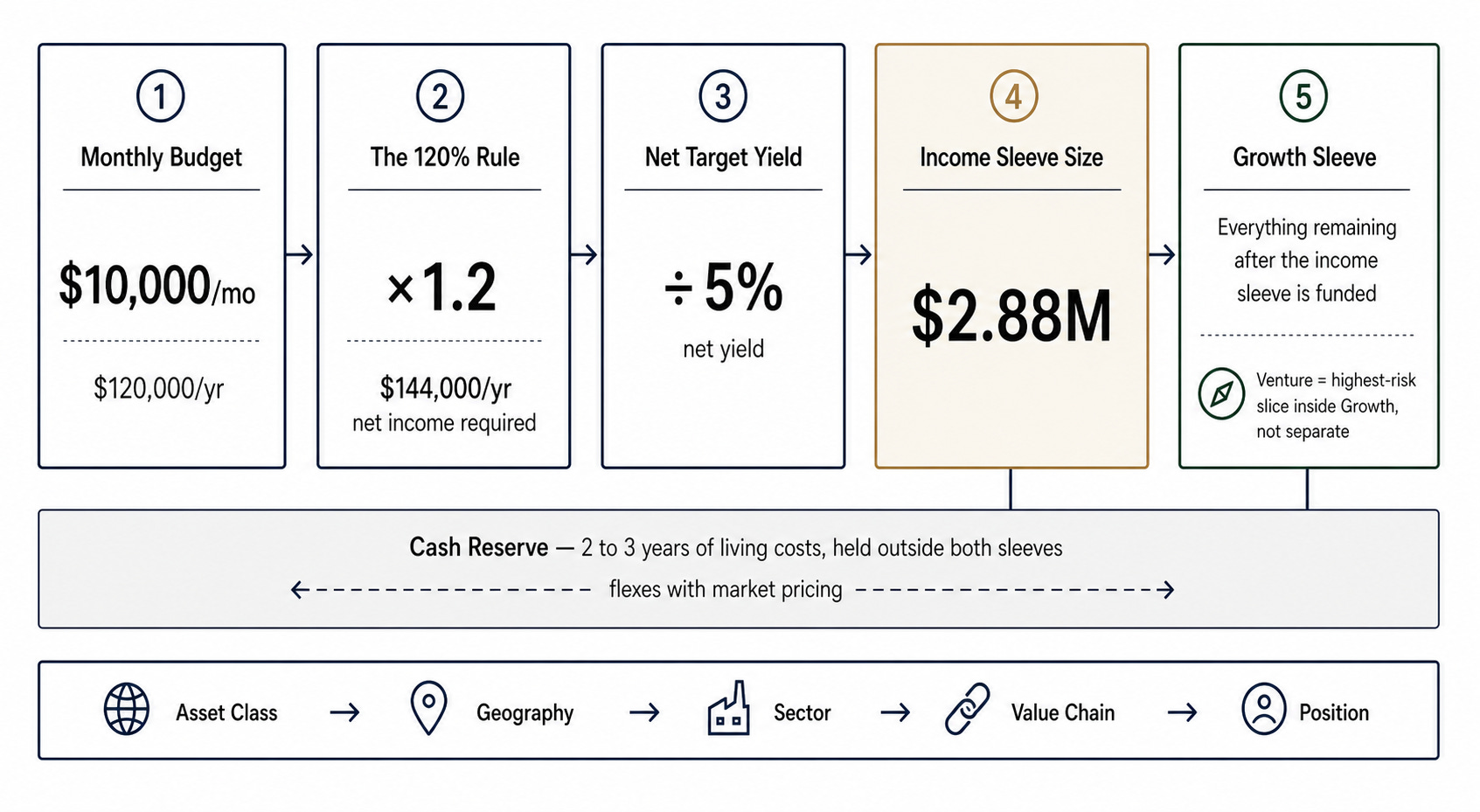

It starts with a number. Not what I would like my life to cost, but what it actually costs. Say the honest figure is US$10,000 a month, or US$120,000 a year. Everything downstream is sized off it, so it has to be real before anything else gets designed.

One rule turns that number into the objective: 120%. The portfolio has to produce not US$120,000 but US$144,000 a year, net, in income alone. The extra 20% is not decoration, even if padding your own income target by a fifth is exactly the sort of thing that gives former CFOs a reputation. It absorbs a dividend cut, a currency move, a year when one holding suspends its payout, without forcing me to sell anything to eat or pay rent. Income that only ever exactly matched the budget would put me straight back to selling at the wrong time in the first bad year, which is the single thing this whole design exists to prevent.

The foundation: strategic asset allocation

Serious family offices don’t start from stocks. They start from a strategic asset allocation: the objective first, then asset classes, then geography, then sector, and only last the individual security. I know, I was CFO at a family office for 6 years, and it is the discipline I brought with me when I left.

For me the top of that allocation is the split itself: an income sleeve, a growth sleeve, and a cash reserve, each sized off the 120% number before a single holding is chosen.

US$144,000 a year is a target, not a portfolio. Turning it into one takes a yield, and the yield is not mine to pick; the rate environment sets what is achievable for a given amount of risk, and it has never once asked what my budget is. Say that environment supports 5%, net of withholding tax, at a risk level I am willing to carry. US$144,000 divided by 5% is roughly US$2.88 million. That is the income sleeve: capital set aside for one job, producing this year’s living expenses on schedule, whatever the market is doing. Move the rate, the risk, or the budget, and the sleeve is rebalanced to match.

Everything not required to hit that objective goes into the growth sleeve, with venture inside it as its highest-risk, longest-horizon slice rather than a category of its own. The split is not a taste for diversification; it is a direct output of the income objective. A bigger budget or a lower achievable yield pushes more capital into income and leaves less for growth. A smaller budget or a higher yield does the reverse.

Cash sits outside both sleeves, 2 to 3 years of living expenses doing 2 jobs. It funds life directly, so neither sleeve is ever a forced seller, and it is dry powder for when the market gets cheap enough to move it in. It flexes: more when the market looks expensive and I want the sleeves carrying less risk, less when opportunity is cheap. More cash buys a racier sleeve. Less cash demands a duller one. There is no free version of that choice.

Position sizing runs by rules set before any name is chosen. In the income sleeve, no single stock exceeds 7% of the sleeve, and the minimum target once I’ve scaled in is 3%, small enough that nothing breaks the income machine if it cuts its dividend, large enough that it still matters. In the growth sleeve, no single name exceeds 5%. Venture is capped at 0.5% a position, and every venture position is sized for zero: I design it to be a total loss, so nothing about how it behaves can touch how I live.

Inside each sleeve the same top-down order runs all the way down: asset class first, then geography, then sector, then where in the value chain the profit actually collects, and only then the individual name.

The geography rung carries the most weight. It clears economies on a competitive-edge test that has nothing to do with which flag I prefer: human capital that is genuinely rising in capability, innovation that shows up in measured productivity rather than graduate headcount, and a government judged on the policy it implements, not the reform it announces. The test earns its place by how much it rejects. A country loses on it when its workforce shrinks faster than rising productivity and urbanisation can offset, when its university system is hollowing out, or when its government reforms on paper every year and implements none of it, however cheap the assets screen.

Where it lands

Right now the top-down order plays out unevenly, on purpose. I go all the way down to individual companies in the US, China, and Singapore, where the research runs deep enough to hold a single name through a bad year. Europe I hold at the sector or regional level, and part of my emerging-market Asia exposure sits in region-level funds, because I have a view on where the profit pools sit but not yet the company-level edge to back one name over a fund.

Large parts of the world map, the Middle East, South America, Canada, Japan, I hold nothing in at all, not because there is nothing there but because I have not done the work. That discipline has a bill: somewhere in the markets I’ve written off, real money is being made in names I’ll never own, and the line between focus and blindness is one I keep having to re-earn. How far down I go on any name just tracks the research behind it. Where I have not done that work, I own the index or I own nothing.

If I can’t say which part of the value chain actually keeps the profit in my largest holding, I don’t have a thesis. I have a position, and a story I tell myself about it.

One rule binds the whole foundation, income and growth alike: no leverage.

Leverage is supposed to buy holding power, and it does the opposite. Borrow against the book and the timeline stops being only mine; it becomes the broker’s too. When the position falls far enough the margin call comes, always at the worst moment because that is when the collateral is thinnest, and a paper loss I could have sat through becomes a sale I have no say in. That is the trouble with borrowed staying power: it belongs to whoever lent it, and they can take it back on the day I most need to sit still.

Income sleeve

The illustrative US$2.88 million figure sizes the sleeve. It says nothing about what sits inside it, and that is where I turn the arithmetic into a portfolio.

I build it as a spectrum: investment-grade bonds at the safe end, high-yield bonds and income equities at the riskier end, with bond and income funds filling the parts where I don’t have a single-name edge. In practice that means positions I have already written up in full, a few examples rather than the whole sleeve: Chinese state banks held as synthetic renminbi bonds, bought for a politically mandated coupon rather than capital gains; 3 Chinese state telcos paying me roughly 6% a year while the state’s AI-infrastructure build matures; European Banks ETF and Singapore REITs in the same band. The mix is whatever clears the net yield target at the least risk I can get away with, and it moves as prices and rates shift.

I judge this sleeve by whether the cheques arrive. A quoted value that wobbles while the income holds is doing exactly what I built it to do.

One layer sits on top of the sleeve, and it is not a second bet. I hold a fair value range for every name I’ve done the work on. As a position approaches the top of its range I trim it or sell calls; as it approaches the bottom I sell puts, or buy more if I still have allocation budget for the name. The options overlay just monetises homework already done: it pays me to wait at prices I’ve settled on in advance.

Growth sleeve

Once the income sleeve is funded and the cash reserve is set, everything left is growth, and it is genuinely free: free to take real risk, free to sit through a multi-year drawdown, free to do nothing for years, because daily life is already paid for out of a different pocket. That freedom is the entire edge I have over professional money managers. The sleeve can afford to be volatile precisely because it is not being asked to feed or house me. Venture, its highest-risk corner, is sized the same way, as capital I don’t need back on any particular timeline.

Inside it the same asset-class logic holds: single names where my research runs deep, index funds where it does not. So the sleeve holds Chinese EV makers on a still-unproven overseas-margin thesis and US enterprise-software names such as ServiceNow and Salesforce, bought during the SaaS sell-off, alongside broad index exposure such as Nasdaq and EuroStoxx 600 trackers where I don’t claim a single-name edge.

That discipline cuts both ways. SK Hynix and Samsung’s HBM business rallied hard while I held nothing. I watched it. I could see why it was working. I still didn’t buy, because I hadn’t done the work, and the rule that keeps bad analysis out of the portfolio keeps out the good stories I haven’t verified too. That one stings more than a loss.

The no-leverage rule protects growth most of all. Everything here I own outright, which is what lets a thesis be wrong for as long as it needs to be before it comes right.

The human part you cannot design away

Structure solves the first half of the problem and doesn’t touch the second. You can engineer out leverage and forced selling. You cannot engineer out being human, and with no salary behind you the human part gets louder, not quieter. When the screen has been red for a fourth month and no pay cheque arrives to remind you that life goes on regardless, the urge to do something, anything, is real and physical. The telcos were off sharply earlier this year. I didn’t sell. I also didn’t add, because I was already at my position limit for the name, and adding would have meant overweighting it past a rule I’d set for myself, not chasing a better price. A few days later the stock rebounded off the lows, and what I felt watching that wasn’t relief at having followed my own rule. It was regret, specific and immediate, for the money I’d just watched walk past me. The rule had already made the decision.

This is where the structure earns its keep. If daily life is funded, a falling portfolio is just a lower quote, not a threat to next month. If there is no leverage, no downtick can force my hand. That is what turns “just hold through it” from a slogan into something an ordinary person can do: the reasons to sell are already gone, so what’s left is only the feeling, and a feeling I’m not obliged to obey is manageable.

This design has met ordinary drawdowns, not a severe one. I have never sat through a 60% peak-to-trough decline on it with no salary, watching 2 to 3 years of cash reserve thin against a fall that won’t end. The arithmetic says that fear overstates the danger. A 60% fall is a fall in the quoted value of the sleeve, not in the cash it pays: a coupon or a dividend is an amount set by the issuer, not a percentage of today’s screen price, so a sleeve built to throw off US$144,000 keeps throwing it off whether the market values it at US$2.88 million or at US$1.15 million. That US$144,000 is 120% of a US$120,000 budget by design, so the first US$24,000 of dividend cuts lands on the 20% buffer, not on my life. Behind it sits 2 to 3 years of cash, US$240,000 to US$360,000 against that same budget, which funds everything outright even if the sleeve stopped paying altogether for that long. A 60% drop doesn’t by itself stop the cheques.

The case I haven’t lived is the one where the drawdown and a wave of dividend cuts arrive together, and the reserve counts down month by month against an income sleeve that has stopped doing its job. I believe all 3 parts absorb exactly that, but a design that has never met its worst case is still a theory, and holding power without a salary or a risk committee can just be stubbornness with better branding.

I built a portfolio to live on, in a rented flat in Turin, for a year exactly like the one I haven’t lived through yet. The holding power came from the design, and a design only proves itself by being tested. Whether mine survives the worst year of my life, I don’t know, and I won’t pretend to. When it is finally tested I’ll write that up too, whichever way it goes. That is the one thing I can’t research my way out of.

As of the date of publication, I hold positions in Geely Automobile Holdings (HKEX: 0175), BYD Company (HKEX: 1211), ServiceNow (NYSE: NOW), Salesforce (NYSE: CRM), Nasdaq 100 ETF (XETRA: SXRV), STOXX Europe 600 ETF (XETRA: LYP6), Bank of China (HKEX: 3988), China Construction Bank (HKEX: 0939), Agricultural Bank of China (HKEX: 1288), China Merchants Bank (HKEX: 3968), China Mobile (HKEX: 0941), China Telecom (HKEX: 0728), China Unicom (HKEX: 0762), and STOXX Europe 600 Banks ETF (XETRA: BNK). Positions may change after publication without notice. Cohong Lane is a periodical publication made generally available to the public; this is disclosure of my positions, not a recommendation to buy, sell, or hold any securities. Full disclaimer · About Philip